Many rural broadband operators are still evaluating expansion plans using traditional metrics: take rates, cost-per-passing, subscriber growth, and long-term return on investment.

The challenge is that not everyone in the market is playing by those same rules anymore.

Some competitors are prioritizing subscriber growth and market share over near-term profitability, changing the competitive dynamics across rural broadband. At the same time, overbuild activity is increasing, deployment costs remain high, and strategic buyers are reshaping the fiber market through consolidation.

That combination is creating a growing disconnect between how many fiber operators think about their business and how the market around them is actually evolving.

According to the Fiber Broadband Association, fiber deployment hit a record 11.8 million new homes passed in 2025. That sounds like great news until you look at what’s happening underneath.

Competition in Rural Broadband Is Changing Faster Than Your Financial Model

Sixteen percent of fiber homes are now served by two or more providers, up from 13% the year before. And it’s not just Starlink.

It’s T-Mobile expanding fixed wireless.

It’s cable operators upgrading to fiber.

It’s overbuilders funded by BEAD grants.

It’s local fixed wireless providers deploying Tarana upgrades to improve performance.

Meanwhile, 88% of fiber deployers expect costs to increase again in 2026. The economics are getting tighter at the exact moment competition is getting fiercer. That’s not a temporary dynamic. It’s a structural shift in the market.

Fiber Valuations Are Signaling a New Phase of Consolidation

Here’s where the data tells an important story.

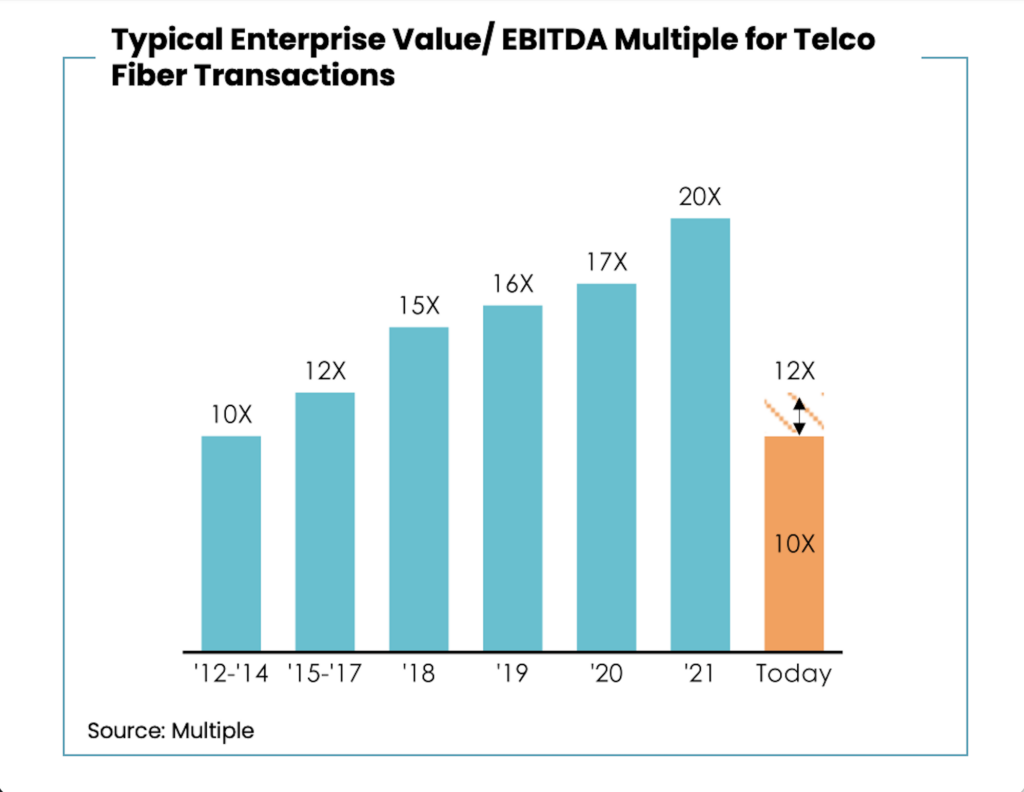

I often share this chart in client meetings with data I’ve assembled from multiple sources and conversations over the years. It captures the entire arc of the market, from where we’ve been to where we are now.

Between 2012 and 2014, fiber transaction multiples climbed from around 10x. By 2021, multiples had reached nearly 20x. Infrastructure funds were in bidding wars. COVID made fiber look like one of the safest investments in the market. Money was cheap, and everyone wanted exposure.

Today, multiples have compressed back to roughly 10–12x. That’s nearly a 50% reset from peak valuations. And depending on the data source, the real compression may be even greater.

If you’re a private equity-backed fiber company that bought in at 16–20x and built your exit model around continued multiple expansion, you’re facing a very different reality today. Many funds have held investments longer than originally planned, hoping operational improvements would help recover those peak valuations. So far, that hasn’t happened at scale.

But there’s another side to this.

For well-capitalized buyers, compressed multiples are creating real opportunities. Strong assets are becoming available at much more rational pricing. And that’s what’s driving the next wave of consolidation.

According to AlixPartners, which surveyed 60 fiber executives and investors:

- 93% say consolidation is either already happening or imminent

- 70% expect it to accelerate over the next year

- Roughly 400 of the 1,900 small-scale U.S. fiber companies are considered meaningful M&A candidates

The buyer mix is shifting as well. Strategic operators, including T-Mobile and Verizon, are acquiring fiber assets that complement their bundled wireless offerings. Of roughly 35 fiber deals in the first half of 2025, the top five transactions were completed by strategic buyers, accounting for more than 80% of total deal volume.

That concentration matters.

Did You Build a Telecom Business or Just Fiber Infrastructure?

Here’s the uncomfortable part.

If you’re a small or mid-sized fiber provider, the next 18 months will test whether you built a business or simply built a network. A network is passings, route miles, and a take rate. A business is a network plus:

- Operational discipline

- Financial health

- Clear strategic positioning

- A customer experience that drives retention and pricing power

I’ve been to many industry events where fiber gets treated as the answer to everything. Build it and they will come. Chase the grant. Add more passings. But fiber is a tool, not a strategy.

The operators struggling today are often the ones who focused almost exclusively on construction and didn’t invest equally in operational excellence, customer retention, and financial management.

Those are the elements that turn infrastructure into a durable, valuable enterprise. The operators who get this right won’t just survive the consolidation cycle. They’ll be positioned to:

- Acquire competitors

- Structure partnerships

- Raise capital on favorable terms

- Or simply run a strong, independent company where selling is a choice, not a necessity

Key Questions Fiber Operators Should Be Asking Right Now

Whether you’re running the company or sitting on the board, this is the moment for an honest conversation.

- Are your take rates truly justifying your capital investment?

- Is your cost structure lean enough for a more competitive environment?

- Do you have a strategic plan beyond “build more fiber”?

- If a buyer approached tomorrow, would you be negotiating from strength or reacting under pressure?

The next chapter of this industry will not be defined by who built the most fiber.

It will be defined by who built real businesses around it.